Construction cost management: A complete guide for 2026

By

Marketing Team

@Onetrace

Construction cost management is the process of keeping spending under control throughout the project lifecycle.

In an industry where tight margins, changing requirements, and unexpected expenses are part of everyday work, effective cost management can make the difference between a profitable project and one that runs at a loss.

But keeping construction projects on budget has never been easy.

According to a 2023 global survey, as many as 75% of these projects exceed their planned budgets, and the outlook for 2026 offers little relief.

Construction professionals expect costs to continue rising, with projected increases of 6.6% and ongoing pressure from material prices, labour costs, supply chain uncertainty, and geopolitical risks.

To help you maintain control in a volatile cost environment, this guide breaks down the principles and practices of disciplined construction cost management.

Key takeaways

Construction cost management is a continuous process, not a one-off task

Costs change throughout a project. Successful contractors plan, track, forecast, and control spending from pre-construction through to final account settlement.Strong cost management protects both profit and project performance

Effective cost controls improve budget accuracy, reduce financial risk, support cash flow, and give project teams the information they need to make better decisions.Early planning and accurate estimating set the foundation for success

Robust cost plans, detailed estimates, realistic budgets, and appropriate contingency allowances reduce the risk of overruns before work even starts.Real-time visibility is critical for controlling costs

Monitoring labour, materials, variations, and plant usage as work progresses makes it easier to identify emerging issues, update forecasts, and take action before problems escalate.The right technology can make cost management significantly easier

Platforms like Onetrace connect labour tracking, material usage, variation management, reporting, and API integrations in one place. With a clearer view of project costs, contractors can make faster, more informed commercial decisions.

What is cost management in construction?

In construction, cost management is the discipline of planning, tracking, and controlling all project-related costs, from initial budgeting to final account settlement.

Its purpose is to keep costs under control without compromising the project’s scope, quality, or delivery timeline.

To do this successfully, contractors need visibility into all major project costs, which are typically classified into the following categories to make them easier to manage and control:

Cost category | Explanation | Examples |

Works costs (hard costs) | Costs directly related to constructing the asset | • Groundworks • Structural steelwork • Concrete and brickwork • MEP installations • Internal finishes |

Fees and statutory costs (soft costs) | Professional, regulatory, and compliance-related costs required to deliver the project | • Architect fees • Quantity surveyor fees • Structural engineering fees • Planning application fees • Building control charges |

Direct costs | Costs that can be assigned to a specific activity or work package | • Trade labour • Subcontractor packages • Material purchases • Task-specific equipment |

Preliminaries (indirect costs) | Costs associated with running and managing the construction site | • Site management staff • Welfare facilities • Scaffolding and temporary fencing • Site security • Temporary power and water |

Fixed costs | Costs that remain largely unchanged regardless of work volume | • Insurance premiums • Software subscriptions • Fixed-rate plant hire • Performance bonds |

Variable costs | Costs that change in line with project activity or scope | • Concrete volumes • Steel tonnage • Fuel consumption • Hourly labour • Waste disposal |

Head office overheads | Business operating costs that support project delivery | • Office rent • HR and finance teams • IT systems • Marketing and tendering costs |

Loss and expense / delay costs | Costs arising from project delays, disruptions, or contractual claims | • Extended site overheads • Idle plant costs • Prolongation costs |

Because these costs can change throughout a project, construction cost management requires continuous attention rather than a single review when the project starts.

Why is construction cost management important?

Construction cost management is important because it helps projects remain financially viable from planning to completion.

Its key benefits include:

Profitability protection: Strong cost controls prevent cost overruns from eroding already tight profit margins.

Budget accuracy: Reliable cost data supports more accurate estimating, forecasting, and financial planning.

Risk reduction: Early visibility into cost issues allows teams to address problems before they affect project performance.

Better decision-making: Real-time cost information enables project teams to make informed commercial and operational decisions.

Cash flow stability: Clear oversight of committed and actual costs allows businesses to manage cash flow more effectively.

Client confidence: Consistent financial performance builds trust and strengthens client relationships.

Stakeholder alignment: Transparent cost reporting gives stakeholders a shared understanding of project finances and progress.

Competitive advantage: Accurate cost management processes support more competitive pricing and stronger bid submissions.

Business resilience: Greater financial control lets firms respond to inflation, supply chain disruption, labour shortages, and other market pressures with greater confidence.

Who is responsible for construction cost management?

Construction cost management is a shared responsibility, with different stakeholders contributing at various stages of a project:

Role | Responsibilities |

Project manager | Oversees the project budget, monitors cost performance, reviews forecasts, and helps ensure financial targets are met throughout delivery |

Quantity Surveyor | Manages cost planning, valuations, subcontractor accounts, change management, and cost reporting |

Estimator | Develops initial cost estimates, pricing strategies, and budget assumptions during pre-construction |

Commercial manager | Provides commercial oversight, manages contractual risk, reviews financial performance, and supports cost control across multiple projects |

Site manager / Site supervisor | Influences costs through day-to-day site operations, labour productivity, programme management, and resource allocation |

Procurement manager / buyer | Sources materials and subcontractors, negotiates pricing, and helps manage committed costs |

Finance team / Cost controller | Tracks actual expenditure, processes invoices, reconciles project accounts, and supports financial reporting |

Client / Developer / Employer’s representative | Reviews budgets, approves major changes, and monitors project costs against business objectives |

Architects and design consultants | Influence project costs through design decisions, specifications, and value engineering opportunities |

How construction cost management works: A step-by-step guide

The eight steps below explain how construction cost management works in practice.

Step 1: Pre-tender cost planning

Pre-tender cost planning establishes the project’s financial framework before work goes out to tender. Accurate planning at this stage reduces the risk of budget overruns later in the project.

Key activities include:

Preparing feasibility and design-stage estimates

Developing elemental cost plans

Reviewing design options through value engineering

Establishing cost codes and budget categories

Benchmarking costs against current market data

Cost plans are often benchmarked against BCIS cost data to verify whether proposed budgets reflect current market rates and identify potential pricing risks before procurement begins.

Step 2: Detailed cost estimating

Estimates convert project requirements into a structured cost model that reflects how the work will be delivered and what it is expected to cost.

To develop this model, estimators quantify the required work using information from drawings, specifications, site investigations, and construction methods. These quantities are then priced using current market rates to produce a detailed cost breakdown.

Particular attention is given to areas where costs are harder to predict, such as groundworks, inflation allowances, and material pricing. This has become increasingly important as ongoing supply chain pressures and market volatility continue to affect construction costs.

A well-developed estimate provides a reliable foundation for tender submissions, project budgets, and commercial decision-making throughout the project.

Step 3: Budget development and contingency planning

A cost estimate may show the anticipated project spend, but a budget defines how that money will be allocated and managed. It establishes spending limits, sets a cost baseline, and provides a framework for tracking financial performance throughout delivery.

A typical construction budget includes:

Project costs allocated to specific cost codes and work packages

Planned spending across different project phases

Cash flow forecasts

Contingency allowances for uncertainty and risk

Contingencies are particularly important because not all risks can be identified during pre-construction. Depending on the project’s stage and level of design development, allowances may be made for design risk, construction risk, unforeseen site conditions, and client-driven changes.

Step 4: Cost control system implementation

A cost control system provides the structure needed to compare actual project performance against the approved budget. The goal is to identify potential issues early enough to take corrective action.

Many contractors use a monthly Cost Value Reconciliation (CVR) process to review:

Actual costs incurred

Value earned from completed work

Budget performance and forecast outcomes

Supporting data is typically gathered from timesheets, subcontractor documents, invoices, retention records, and variation order logs.

Pro tip:

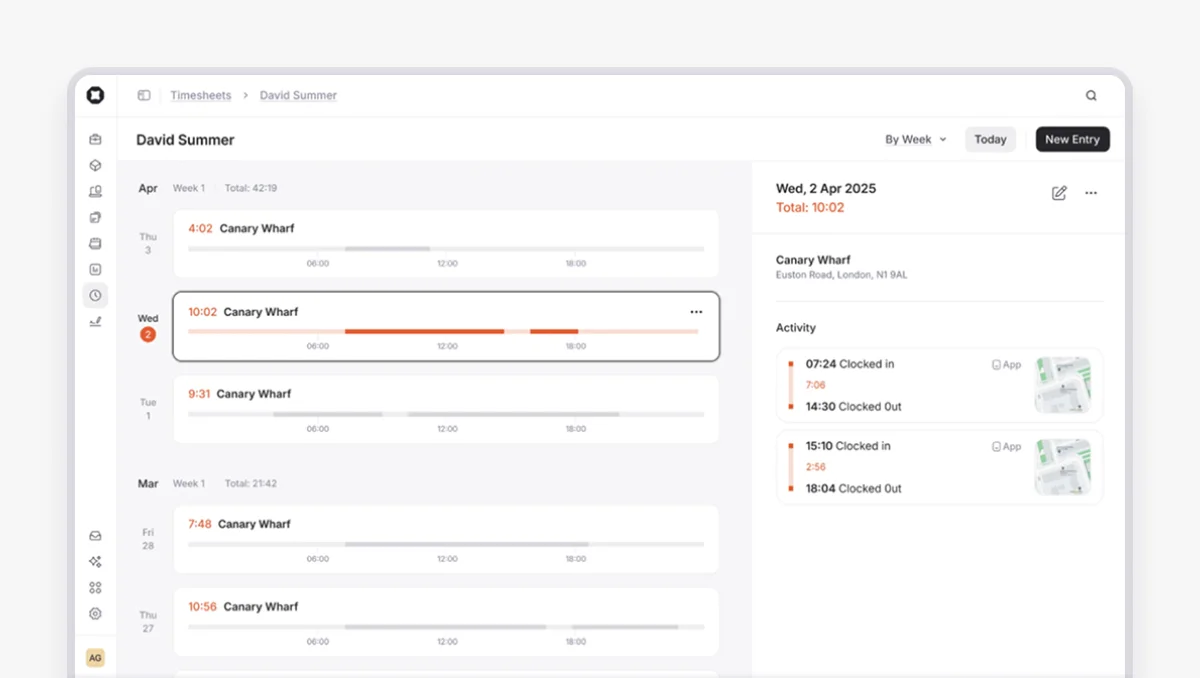

Labour is often one of the largest project costs, so accurate timesheet data plays a key role in cost control.

Onetrace’s Timesheets feature uses GPS-stamped clock-ins and clock-outs to provide a reliable record of hours worked across projects, teams, and individuals.

With live visibility into attendance and labour allocation—plus exportable records for payroll and reporting—contractors can maintain better cost data and support more informed CVR reviews.

Step 5: Real-time cost monitoring

Delays between project activity and financial reporting can create a false sense of security, leaving teams unaware of emerging overruns until invoices or payment applications arrive weeks later.

Real-time cost monitoring helps prevent this scenario by capturing cost-related information as work progresses rather than waiting for month-end reports.

Valuable information to monitor includes:

Labour hours and dayworks

Material deliveries

Variations

Plant and equipment usage

This level of visibility makes it easier to investigate cost variances, assess their impact, and take corrective action while there’s still time to influence the outcome.

Step 6: Variation and change control management

Scope changes are a normal part of construction, but unmanaged variations can quickly erode project margins.

A structured change control process typically includes:

Recording all changes in a variation log

Assessing cost and programme impacts

Reviewing available contingency allowances

Obtaining the required approvals before work proceeds

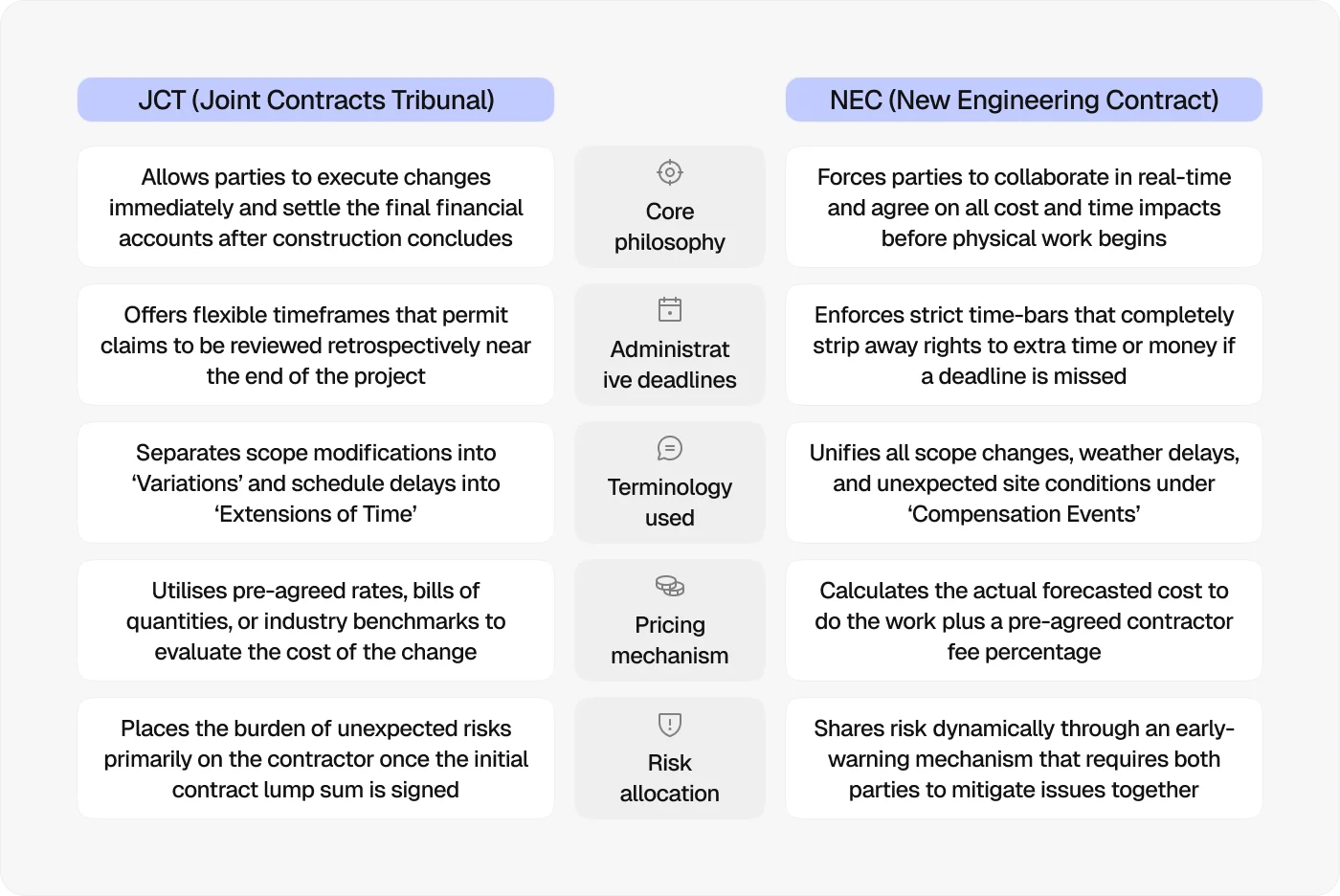

The exact procedures, timescales, and documentation requirements for managing variations will also depend on the form of contract being used. Under NEC contracts, changes are often managed as compensation events, while JCT contracts typically rely on the architect’s or the contract administrator’s instructions.

Whatever the mechanism, prompt valuation and clear documentation help avoid disputes and reduce the risk of falling into the ‘do it now, argue about the cost later’ trap.

Pro tip:

Variations are much easier to manage when they are recorded as soon as they arise.

Onetrace allows teams to flag variations directly within project forms, creating a traceable record of work that falls outside the original scope. This makes it easier to track additional costs, maintain transparency with clients, and produce variation reports that support timely valuation and approval.

Step 7: Ongoing risk assessment and management

Construction projects face a wide range of risks that can affect costs long after the budget has been approved. Robust cost management requires identifying, monitoring, and reassessing those risks throughout the project rather than only during pre-construction.

Many contractors maintain a live risk register covering factors like:

Design changes and incomplete information

Ground conditions and site constraints

Weather-related disruption

Labour availability and wage inflation

Material price fluctuations

Each risk should have a named owner, a defined mitigation strategy, and an estimated cost impact. As risks emerge, evolve, or disappear, project forecasts should be updated to reflect the latest position.

This approach helps teams respond to potential overruns early and maintain a more realistic view of the project’s financial outlook.

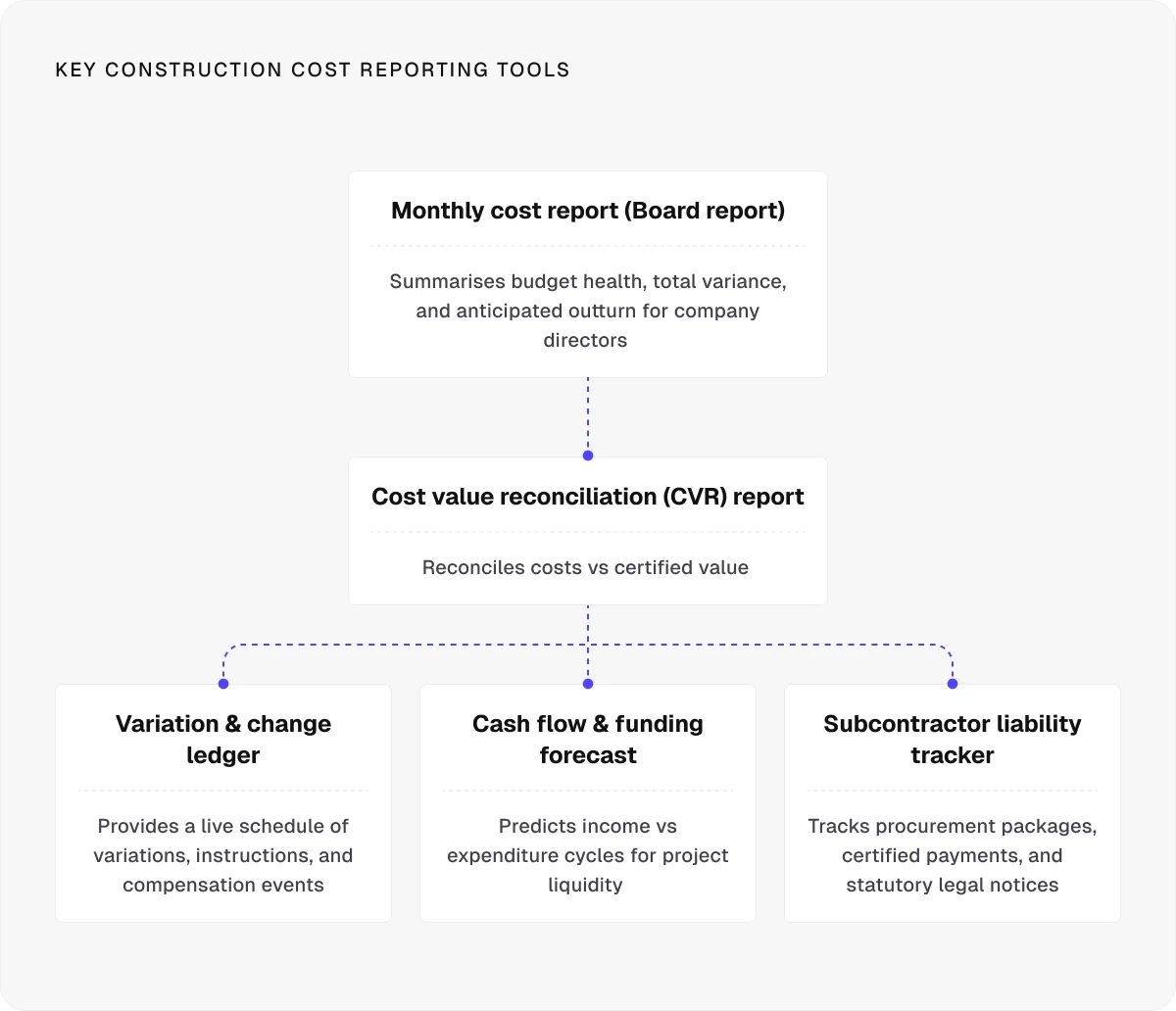

Step 8: Monthly cost reporting

Monthly cost reports consolidate financial performance data in a format that allows stakeholders to understand both the current position and the project’s likely outcome.

While reporting requirements vary, the focus should always be on highlighting issues that require attention rather than simply presenting numbers.

A typical cost report includes:

Approved budget

Actual and committed costs

Forecast final cost

Cost variances

Cash flow projections

Internal reports may provide detailed commercial information, while client-facing reports are often tailored to overall project performance, key risks, and budget position.

Pro tip:

Use red, amber, and green (RAG) status indicators to highlight areas that require attention. A simple visual rating lets stakeholders quickly identify cost, programme, or risk issues without having to review every detail of the report.

How to improve construction cost management: 5 best practices

The following best practices can improve construction cost management and reduce the risk of costly surprises:

Start cost control early: Early commercial input helps identify budget risks and cost-saving opportunities before they become expensive to address.

Monitor cash flow alongside costs: A project can remain within budget while still facing cash flow challenges that affect delivery and profitability.

Maintain regular stakeholder communication: Open communication keeps teams aligned on budgets, risks, and commercial priorities throughout the project.

Use a connected construction management platform: A single source of project data reduces duplication, improves collaboration, and keeps financial information consistent across teams.

Integrate operational and financial systems: Linking project management tools with accounting and ERP software improves data flow and reduces manual administration.

Overcoming construction cost management challenges with Onetrace

Construction cost management is rarely derailed by a single issue. More often, problems stem from a combination of limited cost visibility, delayed site updates, siloed data, poor communication, unmanaged variations, and incomplete records.

The right construction management platform can help address these challenges by connecting site activity, cost data, and reporting in one place.

Onetrace supports construction cost management through features like:

Real-time material tracking: Materials are recorded on site as they are used, with each item linked to predefined rates, providing an up-to-date view of material costs.

Time tracking with GPS verification: Labour hours are captured as work happens, giving teams greater insight into where time is being spent and improving labour cost visibility.

Automatic cost calculations: Material, labour, and service costs are linked to predefined rates, which reduces manual calculations and keeps project costs current.

Live variation tracking: Scope changes can be recorded immediately, making it easier to assess their financial impact and prevent missed variation claims.

Productivity monitoring: Performance data across operatives, teams, and projects highlights inefficiencies that may be affecting costs.

Structured data capture: Custom forms, required fields, photos, and checklists create a consistent approach to collecting project information.

Professional reporting: Detailed project records and reports support payment applications, client communication, audits, and dispute resolution.

API integrations: The Onetrace API connects project data with reporting, accounting, ERP, and business intelligence platforms, reducing duplication and improving data flow across the business.

If you’d like to see how Onetrace supports key cost management activities, book a personalised demo. We’ll walk through the features most relevant to your business, show how they can address your day-to-day challenges, and help you get started quickly if Onetrace is the right fit for your team.

FAQ

What are the 4 types of costs?

The four main types of construction costs are direct, indirect, fixed, and variable costs.

How do you manage construction expenses?

Construction expenses are managed through cost planning, budgeting, cost tracking, forecasting, change control, and regular financial reporting throughout the project.

How do you control costs in a construction project?

Cost control involves comparing actual spending against the budget, monitoring cost variances, managing changes, updating forecasts, and taking corrective action when costs begin to drift from plan.

Marketing Team

@Onetrace

The Onetrace marketing team is passionate about sharing insights, ideas, and innovations that help construction businesses stay connected, compliant, and efficient. Combining industry expertise with a love for clear communication, we aim to deliver content that empowers professionals to work smarter and safer.